Simply Wrong? The Money Multiplier (Part I of II)

The journalist Henry Louis Mencken once quipped: “Every complex problem has a solution which is simple, direct, plausible — and wrong.”

This adage perfectly describes how widely read introductory economics textbooks explain money, banking and monetary policy. They make it seem simple and plausible. There’s one issue, however: they’re wrong. The question, then, is: does it matter? In this short blog post I explain what’s wrong with the way some influential textbooks describe money, monetary policy and banking (including the one we use in this program). In Part II, to be published on this blog somewhere near the end of November, I make the case why more should be done to teach financial literacy, not how to invest for your pension or calculate compound interest rates, but how the plumbing of our monetary system actually works.

Simple, But Wrong

Does it matter whether you learn a theory that is inaccurate (read: wrong)? Not really, right? After all, there are lots of theories that cannot be corroborated empirically. Some theories may have been valid in the past, but in light of new evidence there might no longer be any correspondence between theory and reality. Other theories might rely on unrealistic assumptions, in which case there is no correspondence with reality from the get-go. “So what if theories are wrong?!” one might interject. “We could still learn about all those inaccurate, unrealistic and disproven theories in our courses as examples of wrong theories and move on.” But what if wrong theories are presented to you as valid in your textbook? What if the theory in question is so clearly divorced from reality that even institutional actors who deal with the subject the theory tries to explain on a day-to-day basis say it’s absolute bonkers, encouraging instructors to change the study material?

The theory I have in mind here is taken from economics 101 textbooks—the first texts students come in contact with when studying economics. Unless specifically designed for finance courses, econ 101 textbooks don’t deal in-depth with money, finance and banking, which is astounding in and of itself since we are not living in a world of barter exchange (so money should be pretty prominent in those books—but it isn’t). Still, your off-the-shelf textbook will have chapters that briefly address money (its functions), monetary policy (how money is managed in modern economies today) and the role of banks (what their role is in our economy and in the process of money creation).

One such theory that ties money, banks and monetary policy together is the money multiplier. It roughly says that the level of reserve requirements determines the amount of credit and money in an economy. The formula is fairly easy (Amount of credit = initial reserves * (1/Reserve Requirements)) and so is the intuition behind it: just assume that there is some fixed amount of money in circulation usually found in a shoebox under someone’s bed. Say that shoebox belongs to a person (let’s call him Jan), who goes to a bank to deposit his money (€100 in cash). The bank takes Jan’s €100, credits his account with that amount, puts 10% of that money in reserve and lends out the remaining €90 to Jolanda, who in turn wants to buy a pair of Bluetooth earphones. Jolanda pays €90 for her earphones, the seller puts those €90 in a bank, and the bank keeps 10% in reserve and lends out the remaining €81 to Joris and so on. This way the initial €100 of Jan can be “multiplied” through continuous rounds of depositing and lending, while each deposit is backed up by 10% reserves. At the end, when the last cent has been put into reserve, the amount of money in circulation has multiplied from an initial €100 to a €1000.

It’s an arrestingly simple theory that sounds logical and appealing (and it’s easy to memorize for an exam, I guess). The only problem with that theory is that it’s wrong—plain and simple.

Money Out Of Thin Air…

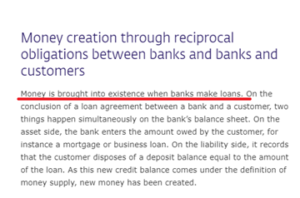

What’s wrong with the money multiplier? Everything! Most of the money we use in our economy in day-to-day transactions is created by commercial banks when they make loans. But where did that money come from in the first place? The textbook answer would be: from deposits. Jan, in our example above, made a deposit first before Jolanda was able to get a loan—where Jan got the cash in the first place is not addressed. Presumably from the central bank who issued the notes—which, as you will see in a moment, only adds to the confusion as to what type of money central banks issue, who can hold this money and whether it is actually lend out. Outside the imaginary economy of our textbooks the answer would be: from the keyboard of whoever is responsible for issuing a loan at the bank, that is money was created “out of thin air.”

Contrary to what the textbook says (or tries to insinuate): banks don’t lend out deposits (nor do they lend out reserves). Instead, banks create deposits whenever they make loans. This very simple insight seemingly defies both economic logic and, for some at least, a sense of justice. As Professor of Economics Perry Mehrling wrote: “This process apparently offends common sense understanding of what it means to make a loan—I can only lend you a bicycle if I already possess a bicycle.” A quick search on the Internet will cause further puzzlement. You might discover that lots of countries (UK, Canada, New Zealand) have no reserve requirements at all. What’s the money multiplier in those economies? Infinity? Are they all free to create as much credit / money as they want? Do they? Hardly. So other things than reserve requirements seem to matter – the money multiplier cannot explain this.

You could say: “Well, it’s a U.S. textbook so what is written there applies to the US only.” Yet, another five minutes of googling and you find out that there have not been any reserve requirements for retail deposits since last year in the US either. A more thorough search might direct you to the websites of various central banks, most of which have a section on how money is created. The story told in these explainers is more or less the same, namely: banks create money when they make loans, and there is no such a thing as a money multiplier (see here, here, here, here). A similar story is provided by people working in finance (see here).

There is thus consensus that banks create money when making loans. They don’t lend out deposits, they don’t lend out reserves to customers in the form of loans, nor do they have to wait for deposits to come in in the first place. To be sure: banks can fund loans with deposits, and depending on the interest rates on the interbank markets, it is probably a cheap way to do this. But they don’t have to a) wait for deposits to come in first; and b) they can use other ways to fund the loans.

…But Not Alchemy

The difficulty of accepting that money creation works this way (and seems like alchemy) stems from the fact that economics textbooks conceive of money as a veil over barter, as a thing that facilitates exchange and is always available for that purpose when needed. But money, whether in the form of deposits, money market fund shares or stablecoins or what have you, is not a thing (e.g. a bicycle). What we consider money in our everyday transactions (mainly deposits) is actually just a claim we hold against someone else (e.g. a bank) of being paid “real” money (cash) on demand at some point in the future (maybe today, maybe tomorrow, maybe next week). With physical cash and coins being slowly replaced by all sorts of electronic means of payment (at least in parts of the world) that claim on being paid real cash (for individuals) also wanes—which brings into sharper relief the hierarchical nature of money.

Seen from this perspective, both loans and deposits are mere promises of future payments (either central bank money between banks or cash/coins from banks to customers). But if money is nothing but relations between different entities that make claims and counter-claims against each other (claims on some future payment), then it is better to conceive of money as an institution, rather than a commodity or a thing. And part of what makes an institution an institutions it that individuals take it for granted, that they trust it for its own sake.

Which brings me to the following question: Does it matter if the textbook story about the money multiplier (and money) is so divorced from reality? It does for a number of reasons, which I will address in Part II.